Imagine a corporate treasurer logging into a dashboard and seeing not only their own transactions, but those of every competitor, supplier, and customer - fully visible and permanently recorded.

This is effectively how public blockchains operate today; they are public by default.

That means if someone pays a business using a public blockchain like Solana or Ethereum, anyone can potentially view wallet balances, transaction amounts, payment history, counterparties and broader trading patterns.

For businesses and consumers, that creates a level of financial transparency that would be unacceptable in traditional banking.

Imagine a competitor analyzing supplier payments, a customer’s spending history becoming traceable, or high-net-worth clients exposing treasury activity simply by transacting.

Traditional finance was not designed this way. Your bank account activity is not searchable on the open internet. Public blockchains changed that assumption.

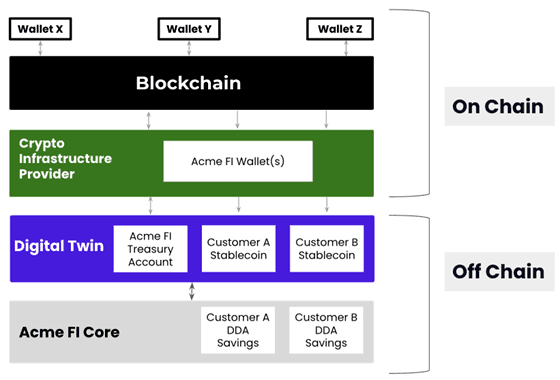

This is where Digital Twin infrastructure becomes strategically important for banks: a real-time authorization ledger that separates blockchain settlement from customer identity and transactional visibility.

The Missing Layer in Stablecoin Adoption

Stablecoins solve many problems like instant settlement, programmable payments, lower cross-border friction and 24/7 money movement.

But privacy remains one of the biggest barriers preventing banks and enterprises from fully embracing on-chain payments. A bank cannot realistically tell commercial clients: “Your transactions settle instantly, but anyone can inspect them forever.”

That is not a viable model for corporate treasury, wealth management, payroll, or institutional finance.

Banks need the benefits of stablecoins without exposing client financial activity to the public blockchain.

Privacy and Compliance Can Co-Exist

Traditional banking systems have always balanced customer privacy with regulatory oversight.

Banks are expected to:

- verify customer identity (KYC)

- monitor suspicious activity (AML)

- comply with sanctions requirements

- support audits and regulatory reporting

But, that oversight is limited to authorized parties - not the general public.

Public blockchains changed that model by making transaction activity broadly visible by default. While transparency can support network verification, it creates challenges for businesses and financial institutions that are expected to protect sensitive financial activity.

As stablecoin adoption grows, banks will need infrastructure that preserves regulatory compliance while limiting unnecessary public exposure of customer transaction data.

Why Digital Twin Matters

Deploying Digital Twin in a bank’s infrastructure allows banks to separate public blockchain settlement from customer identity and transactional privacy.

Instead of exposing raw customer activity directly on-chain, banks can abstract wallet infrastructure, shield identities, and maintain compliant privacy controls.

The result is a system where customers still benefit from stablecoin rails, banks retain compliance oversight but external observers cannot map every financial interaction.

In other words, Digital Twin enables stablecoin usability without forcing too much transparency onto bank customer transactions and balances.

The Next Phase of Stablecoins

The next generation of financial infrastructure will not be won solely by speed, settlement efficiency or lower fees. It will be won by platforms that combine blockchain efficiency with institutional compliance and privacy.

Privacy-aware infrastructure - like Digital Twin - is what makes stablecoin banking viable for real-world financial institutions and their customers.